The Invisible Raise-Eater: Why Your Success is Leaving You Broke

So, you got a promotion last year. It wasn’t a “retire on a yacht” kind of bump, but it was significant—enough that you finally felt like the breathing room had arrived. You started thinking, “Okay, this is it. Now I can actually start building a real war chest. No more living paycheck to paycheck.”

Spoiler alert: You didn’t.

Three months into that new salary, you find yourself staring at your bank statement, genuinely confused about where the delta went. It’s not like you bought a Ferrari. It’s more subtle than that. You start buying lunch out three times a week instead of packing a sandwich. You upgraded to the “nice” coffee spot because, hey, it’s only two bucks more and you’re a Senior Manager now. Then, somehow, rent starts feeling tight again. Food delivery becomes a Tuesday night reflex rather than a monthly treat.

Sure, you weren’t the only one feeling this. Many years ago, I remember getting the annual end of year bonus at a company I was working at and while I was directing mine towards investments, something, I had mentioned to a coworker, and he literally laughed in my face. “Dude,” he said. “I got a 15% raise this year, and a great bonus and my life looks exactly the same financially. I just have more cardboard boxes in my recycling bin and new pickup.”

And while this wasn’t the first conversation we have had about finances, it certainly made me more acutely aware of priorities and the havoc the lack of financial discipline can wreak on our lives. This was structural failure and something I wanted to avoid.

The Psychology of “Deserving”

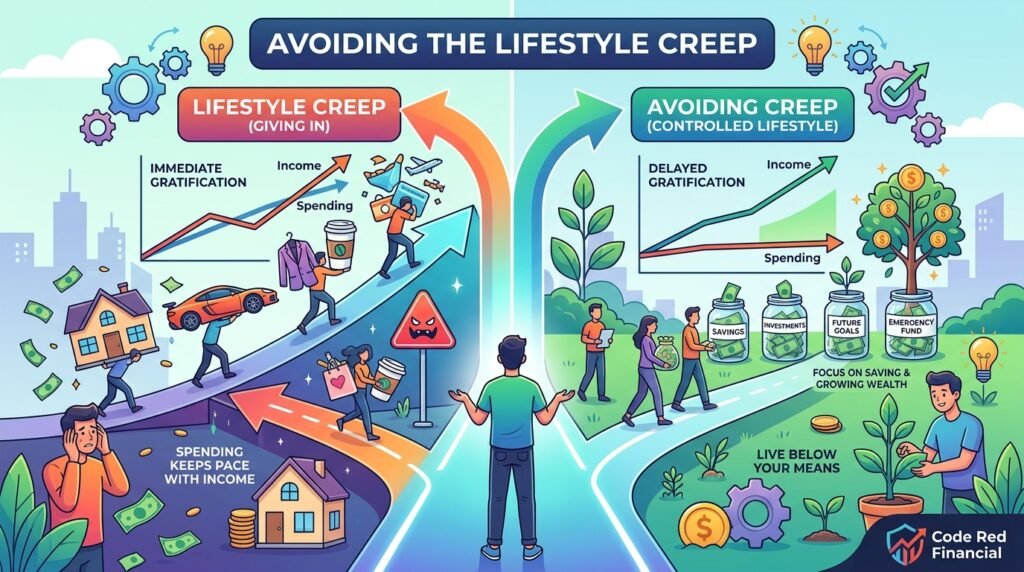

What we’re talking about is a phenomenon where your spending grows at the exact same velocity as your income. It’s not a conscious decision. You don’t sit down and say, “I’m going to blow this entire raise on overpriced salads and streaming services.” It just… happens.

The logic is seductive. You make more money, so nicer dinners feel “normal” now. You’re earning more, so you “deserve” that apartment with the better view or the car that doesn’t require a prayer and a jump-start every Tuesday. Each individual purchase feels entirely rational in the moment. You’ve worked hard; shouldn’t your life reflect that?

But here’s the trap: when you add it all up, you’re right back where you started. Your new income has vanished into the ether. You’re back to feeling “middle-class broke” despite making significantly more than you were two years ago. The sneakers are nicer, the coffee is better, but the bank account is just as stagnant.

The sneakiest part is that it’s invisible. There’s no “A-ha!” moment where you realize you’re sabotaging yourself. It just silently eats your raises until you check your account and wonder what the hell happened to that money you were supposed to be saving for the big stuff.

Why You Should Actually Give a Damn

Look, I’m not saying you’re headed for the poorhouse. You’re making good money. But that’s exactly why this is so dangerous.

When your expenses rise to meet your income, your savings don’t actually grow. Your retirement date gets pushed back another five years every time you “upgrade” your life. You end up stressed about money despite a solid paycheck, and one unexpected medical bill or car repair wrecks your entire month.

But the real killer? It’s the “Golden Handcuffs.” You’ve built a life that requires every single dollar you make just to maintain the status quo. You can’t quit the job you hate. You can’t take a risk on a new business. You can’t move to a city you actually like. You’ve traded your freedom for a nicer upholstery package and a better ZIP code. The real cost isn’t the $7 latte; it’s the fact that you’ve unknowingly traded away your ability to say “no.”

How to Defeat the Creep

The good news is that you don’t need to move into a van and eat lentils for the rest of your life. You just need to stop operating on autopilot. Here is what actually works in the real world.

1. Intercept the Capital at the Border

This is the only tactic that really matters. When you get a raise or a bonus, you need to decide what happens to that money before it ever touches your checking account. If your paycheck goes up by $500, tell yourself: $350 goes straight to the brokerage or savings account, and $150 is for me to enjoy guilt-free. Set it up to happen automatically. If you never see the money, you won’t miss it. You still get to celebrate the win, but you’re protecting your future self first.

2. Plan Your Upgrades (Don’t Stumble Into Them)

Most people stumble into lifestyle upgrades by accident. Change the script. When you get a raise, deliberately set aside 10% of it for “lifestyle improvements.” New clothes, better dinners, whatever makes you happy. Put it in the budget on purpose. When you plan the splurge, you get the satisfaction without the “where did my money go?” hangover.

3. Figure Out What “Enough” Actually Means

This was the game-changer for me. Sit down and be brutally honest: What kind of apartment do I actually need? What car would actually make my life better, not just fancier? What am I buying just because it’s what people in my tax bracket are “supposed” to buy? Once you define your own version of “enough,” it becomes much harder for the marketing machines and Instagram feeds to tell you what you’re missing.

4. The “Fixed Cost” Fortress

Rent, mortgages, car payments, and insurance—these are the “Big Four.” They are incredibly hard to cut back once you’ve committed to them. Don’t bump them up just because your paycheck got bigger. Your current apartment was fine last year; it’s still fine today. Keep your fixed costs lean, and you create “the gap”—the space between what you earn and what you spend. That gap is where actual wealth is built.

5. The 30-Day Rule

I’m dead serious about this. Want the new iPhone? Want the $400 boots? Put it on a list and wait 30 days. Most of the time, the dopamine hit of the idea of the purchase wears off before the month is up. If you still want it after 30 days, and it fits the budget, buy it. You’ll find that 80% of your “must-haves” vanish when given a little time to cool off.

6. Celebrate Without a Receipt

You crushed a project? Celebrate. But stop equating “celebration” with “spending money.” A day off, a long hike, a home-cooked meal with friends—these things often provide more actual satisfaction than a $200 dinner that leaves you feeling bloated and regretful the next morning. When you break the habit of celebrating with your credit card, you win.

It’s Not About Restriction—It’s About Intention

This isn’t about being a miser, although I must admit that frugality runs in my blood, but being the architect of your own life will determine your outcome in just about anything you choose to do. So, when you elect to spend your hard-earned money on things that actually matters, you don’t feel deprived, as a matter of fact and this is my own experience, the feeling empowerment is the outcome.

You’re saying “yes” to the life you actually want, not the one that your social circle or your feed told you to want, and I do understand the social stigma pr pressures of adhering to a particular lifestyle while tuning out the noise of the “buy” “buy” society we are in but it is possible to enjoy your life and success without satisfying the expectation that often is attached to higher income individuals. Listen, buy nice things, celebrate your wins. but simply do it with a purpose.

That shift—from “this just happened to me” to “I decided this”—changes everything. Your money becomes yours again. Your future stops being a scary question mark. And most importantly, you get your freedom back.

That’s the whole point, isn’t it?

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Consult with a qualified financial advisor or tax professional before making any decisions about your investments or retirement accounts.