And the Truth That Will Set You Free

Every so often I am inclined to share misnomers we all have and today I is one of those times, here we go. Have you ever stopped to ponder many popular urban myths you have been told about many, some of which you or dare I say we have embraced about money, not because we are gullible, but because these myths are everywhere. They’re passed down from well-meaning parents, repeated by broke friends, and reinforced by a society that profits from keeping you financially stressed.

I’ve spent years untangling my own relationship with money, and I can tell you firsthand that breaking free from these myths is the difference between living paycheck to paycheck and building real wealth. So, let’s cut through some of the rubbish and expose the money myths that are quietly draining your bank account and restricting your financial growth.

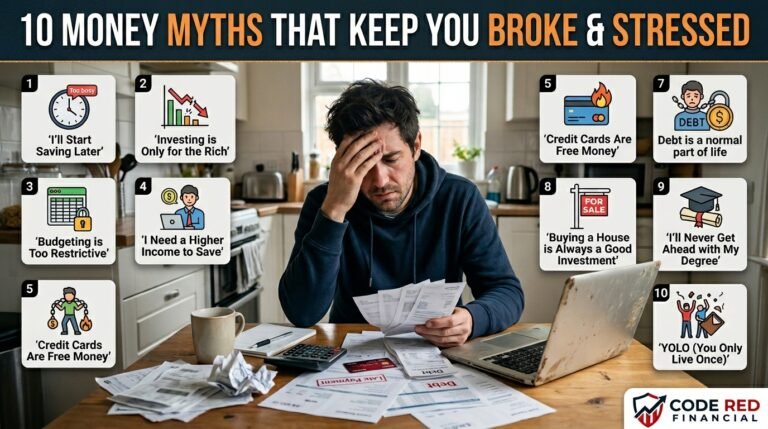

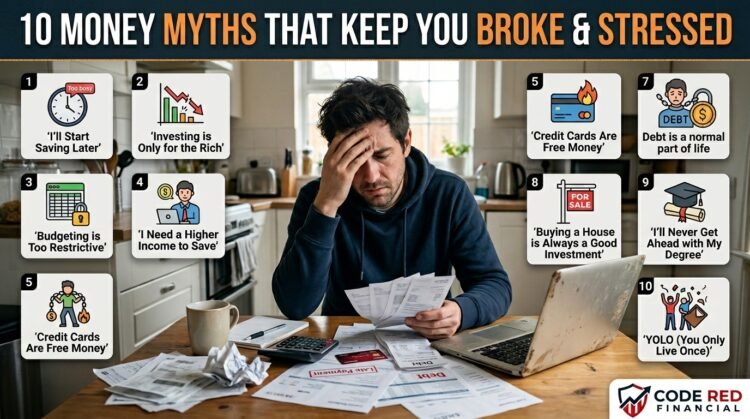

Myth 1: You Need to Make More Money to Build Wealth

Here’s a shocker: your income isn’t the only problem; your money habit is.

I know someone who makes six figures and still lives paycheck to paycheck. I also know people earning modest incomes who’ve built impressive nest eggs. The difference? Intentionality. The person making $150,000 believes their income entitles them to a luxury apartment, new car payments, and weekend brunches that cost more than some people’s grocery budgets.

Wealth isn’t about how much flows in—it’s about how much you keep. Before you chase that promotion or side hustle, look at where your current money is going. You might discover you’re already making enough to build wealth, you’re just letting it slip through your fingers.

The real deal: Wealth building starts with managing what you have, not earning more to waste more.

Myth 2: A Car Payment Is Just Part of Life

Somewhere along the way, we normalized going into debt for a depreciating asset. Let that sink in. You’re borrowing money to buy something that loses value the moment you drive it off the lot.

The average car payment in America is over $700 a month. That’s $8,400 a year you’re handing over for the privilege of driving something you don’t actually own. Imagine investing that money instead. In 30 years, at a modest 7% return, you’d have over $850,000. That’s nearly a million dollars traded for decades of car payments.

I get it—you need reliable transportation. But you don’t need a $40,000 car with heated seats and a sunroof. A $10,000 used vehicle will get you to work just fine, and the freedom from that monthly payment will change your life. I must admit, I detest car loans and have avoided them for the longest of time. As a matter of fact, my propensity for figuring out how things work and fixing stuff stretches back to my early childhood and has served me well when it comes to working on my vehicles and in many other areas of my life.

The real deal: Car payments aren’t inevitable. They’re a choice that keeps you broke while the dealership gets rich.

Myth 3: Credit Cards Are Evil

This myth swings too far in the opposite direction. Credit cards aren’t evil—they’re tools. And like any tool, they’re only dangerous when you don’t know how to use them.

People who swear off credit cards completely often have poor credit scores, which costs them thousands in higher interest rates on mortgages and insurance. Meanwhile, those who use cards strategically earn cash back, build excellent credit, and enjoy fraud protection that debit cards simply don’t offer. Renting a car for instance is easier with a major credit card, along with the insurance it provides. Dave Ramsey, for example, isn’t a fan of credit cards, and honestly, in most cases, neither am I. However, there are times when they come in handy—not as a quick cash fix, but as a tool for transaction benefits.

The key is treating your credit card like a debit card. Only spend what you already have, and pay it off in full every month. No exceptions. Do this, and you’ll harvest all the benefits while avoiding the debt trap.

The real deal: Credit cards are powerful allies when used with discipline, not enemies to be feared.

Myth 4: You Can’t Get Ahead on a Low Income

This is the myth that keeps millions stuck in place, believing change is impossible. It’s not.

Yes, building wealth is harder on a low income. I won’t pretend otherwise. But harder doesn’t mean impossible. Some of the wealthiest self-made millionaires started with nothing. The difference? They refused to accept their current circumstances as permanent.

On a tight budget, every dollar matters more, which forces you to be more intentional. This discipline becomes a superpower. You learn to distinguish between wants and needs. You get creative. You find ways to increase income, even if it’s small at first. The person making $30,000 who saves 10% is building the habits that will serve them when they’re making $60,000.

The real deal: Your starting point doesn’t determine your destination. Your habits do.

Myth 5: Investing Is Only for Rich People

This myth probably costs people more money than any other on this list. Because while you’re sitting on the sidelines thinking the stock market is a rich person’s game, inflation is quietly destroying your purchasing power.

You can start investing with literally $5. Apps like Acorns, Robinhood, and even traditional brokerages have eliminated minimum investment requirements. The barrier to entry has never been lower, yet people still believe they need thousands to get started.

Time in the market beats timing the market, every single time. Someone who invests $100 a month starting at age 25 will have more at retirement than someone who invests $200 a month starting at age 35. The early bird doesn’t just get the worm—they get compound interest, the most powerful force in finance.

The real deal: You don’t need to be rich to invest. But you do need to invest to become rich.

Myth 6: Buying a Home Is Always Better Than Renting

The pressure to buy a home is intense. Family members ask when you’re going to stop “throwing money away on rent.” Society treats homeownership as the ultimate sign of adulting. But the math doesn’t always support this narrative.

When you rent, you’re paying for flexibility, predictability, and freedom from maintenance costs. When you buy, you’re paying for mortgage interest, property taxes, insurance, repairs, and the opportunity cost of the down payment you could have invested elsewhere.

Run the numbers for your specific situation. In many expensive coastal cities, renting and investing the difference can leave you wealthier than buying. Sometimes the smartest financial move is the one that doesn’t fit the traditional script.

The real deal: Homeownership isn’t always the wealth-building move it’s cracked up to be. It depends on your market, lifestyle, and opportunity costs.

Myth 7: Budgets Are Restrictive and Depressing

People hear the word “budget” and immediately think of deprivation. No more lattes, no more fun, just a joyless march toward financial responsibility.

That’s backward. A budget isn’t about restriction—it’s about permission. It’s a plan that tells you exactly what you can spend guilt-free because you’ve already allocated money for your priorities. Without a budget, every purchase carries a nagging voice asking, “Can I really afford this?” With a budget, you know the answer.

The best budget is the one you’ll actually follow. Whether it’s zero-based budgeting, the 50/30/20 rule, or just tracking your spending for awareness, the format matters less than the habit. Start simple and adjust as you go.

The real deal: Budgets create freedom by eliminating financial anxiety, not by restricting your life.

Myth 8: I’ll Start Saving When I Earn More

This is the cousin of Myth #1, and it’s just as destructive. The belief that you’ll magically become better with money once you earn more is a fantasy. Research consistently shows that income and spending rise together—a phenomenon called lifestyle inflation.

You won’t suddenly become a saver when you get that raise. You’ll become a person who makes more and spends more. The time to build the habit of saving is right now, even if it’s just $20 a month. Because the habit is what matters, not the amount.

Start where you are. Save something, anything, every single month. As your income grows, your saving muscle will be strong enough to actually capture that growth instead of watching it evaporate into nicer stuff.

The real deal: Savers save regardless of income. Start now, even if small, or you never will.

Myth 9: Debt Is Normal and Unavoidable

Credit card debt, car loans, student loans, personal loans—we’re swimming in debt and calling it normal. But normal and healthy aren’t the same thing.

Consumer debt is a relatively modern invention. Your grandparents probably didn’t finance furniture or put vacations on credit cards. They saved up and paid cash. Somewhere along the way, we started treating future earnings as current spending money.

Some debt can be strategic—a mortgage on an appreciating asset, student loans that increase your earning potential. But most consumer debt is just impatience in financial form. You’re borrowing from your future self to satisfy your current self, and future you will resent it.

The real deal: Debt might be common, but it’s not inevitable. Living below your means and saving for purchases is still possible, just unfashionable.

Myth 10: Money Can’t Buy Happiness

And why not sum this all up with the big one. People love to say money can’t buy happiness, usually while struggling to pay rent or avoiding medical care because of the cost, perhaps it is a psychological defensive mechanism to make us better about not having as much of it as we desire, but that is just my unscientific opinion.

The research is clear: money absolutely can buy happiness, up to a point. That point is when your basic needs are met, you have financial security, and you’re not stressed about bills. Beyond that, more money has diminishing returns on happiness.

But here is a fact—most people reading this haven’t reached that point yet. If you’re worried about making rent, skipping doctor appointments, or losing sleep over debt, more money would absolutely improve your happiness. Not because money is the source of joy, but because financial stress is miserable and that is simply putting it lightly.

The real wisdom isn’t that money can’t buy happiness. It’s that money buys freedom from the things that make you unhappy—and that freedom creates space for joy and why would anyone not desire a little bit more freedom?

The real deal: Money can’t buy happiness directly, but it can eliminate the financial stress that destroys it and that has wreaked havoc on the lives of so many.

Breaking Free

Breaking free from these myths won’t happen overnight. They’re deeply embedded in how we think about money, reinforced by years of repetition and societal pressure. But awareness is the first step.

Start small. Pick one myth that resonates most and challenge it in your own life. Maybe it’s finally creating that budget, or starting to invest with just $20, or rethinking whether you really need that car payment.

The people who build real wealth aren’t smarter than you. They’re not luckier. They just stopped believing the lies that keep everyone else broke. Your turn to do the same.

What money myth has held you back the longest? Which one are you ready to finally break free from? The answers to those questions might just change your financial future. If you made it this far, congrats, when I sat down to compose this article, I had to restrained myself from making it a graduate thesis, because of how much the topic means to me.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Consult with a qualified financial advisor or tax professional before making any decisions about your investments or retirement accounts.